President-elect Donald Trump has made clear his fondness for fossil fuels, a fondness that was reciprocated by many in the industry. Expectations are high. But what does support for the US oil sector mean in practice? And how might America’s oil-producing friends in the Middle East receive the Trump administration’s oil market and diplomatic priorities? This policy analysis explores how the “Trump effect” might play out.

One of the more certain policies of the incoming administration is support for increased US oil and gas production, a staple of the President-elect’s campaign. Yet American oil and gas companies’ willingness to increase production depends more on signals from the market than those from the president and federal government.

Indeed, the president can cajole, deregulate, lease drilling acreage, and if Congress cooperates, even change laws. But if market indicators point in the opposite direction, most oil company CEOs will find ways to ignore the federal government. With US oil output hitting record highs this year on President Joe Biden’s watch, US oil investors continue to favor capital discipline over production increases as a corporate strategy.

Support for increased US oil and gas production is a staple of Trump’s campaign.

Making Trump’s choices more difficult is the roughly even split between American economic interests that benefit from high oil prices and those benefiting from lower prices. The oil sector and its financial providers win when prices are high, and the manufacturing and transportation sectors (and consumers) gain when they are low.

Even automobile fuel efficiency standards, a likely Trump target after being tightened by Biden, are another double-edged sword. Unwinding fuel efficiency and electric vehicle supports would find backers in the oil business—and probably a few carmakers—but doing so would eventually increase US gasoline demand, emissions, and prices. Additionally, reduced vehicle efficiency would increase US motorists’ exposure to geopolitical risk. The less efficient a vehicle, the more its owner is invested, consciously or not, in stable fuel prices and avoidance of threats to the free flow of oil through the Strait of Hormuz. The second Trump administration’s likely intensification of pressure on Iran could indeed exacerbate such risks.

OPEC’s ‘Coping Mechanism’ for More American Oil in the Market

Trump’s exhortations to drill more American oil—if heeded by the US oil sector—could create frictions with Saudi Arabia and other US friends in the Organization of the Petroleum Exporting Countries (OPEC) cartel. Since the shale revolution kicked off around 2007, OPEC has steadily lost market share to the United States (Fig. 1). American supply overtook Saudi Arabia’s in 2014 and has reached record levels under Biden.

Figure 1: US oil production has climbed relentlessly since the shale revolution, while Saudi Arabia and “core” OPEC production has largely held steady. Chart includes oil and natural gas liquids (NGLs). (Source: Energy Institute 2024)

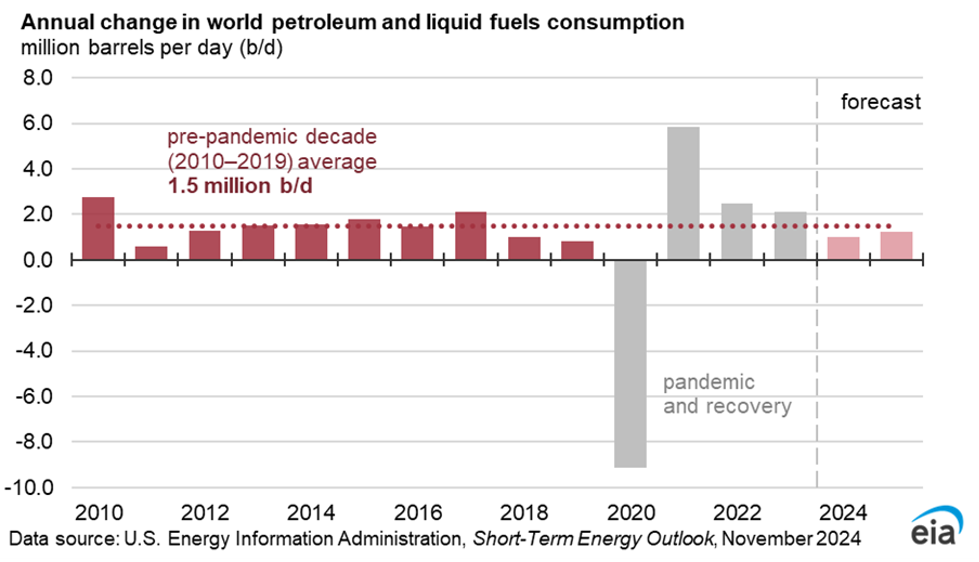

If global oil consumption were growing strongly, OPEC and Saudi Arabia might find US competition less worrisome. But global demand growth has slowed. The US Energy Information Administration forecasts an increase of one million barrels per day (b/d) in oil and NGL demand this year, and 1.2 million b/d in 2025. Both are below the pre-pandemic 10-year average of 1.5 million b/d of annual growth (Fig. 2).

Figure 2: Oil demand was lagging historic growth levels in 2024 and is forecast to remain slightly lower in 2025 (Source: EIA 2024)

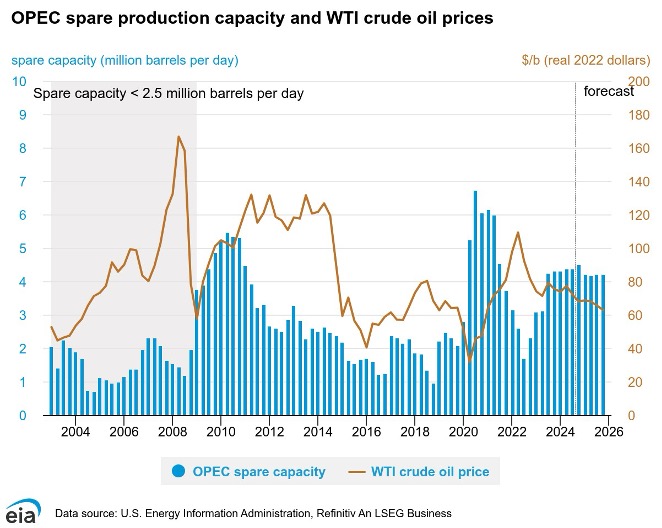

So-called core OPEC still harbors more than 4 million barrels per day of spare, or unused, oil production capacity, with even more held by Russia and the remaining OPEC+ members (Fig. 3). Members like the United Arab Emirates (UAE) are agitating to bring that spare capacity on stream. One of the factors holding OPEC back is that global oil demand is too weak to soak up additional oil coming from the United States and other non-OPEC producers such as Brazil, Canada, Guyana, and Norway.

Figure 3: OPEC had more than 4 million b/d of spare oil production capacity in 2024 (Source: EIA 2024)

At some point, Riyadh may revert to a “price war”—raising output to drive out higher-cost competitors—to make upstream oil investment in the United States and elsewhere less attractive. If Trump follows the playbook suggested by his campaign rhetoric, and American producers raise output, a price war with OPEC becomes more likely. The resulting cratering of prices would damage the interests of all producers, although one might imagine Trump leveraging the upside by taking credit for low gasoline prices.

Contrasting Gulf Relations Under Trump and Biden

Another area where assumptions about Trump’s agenda may be incorrect is in US foreign policy and the interests of oil-exporting countries in the Arabian Gulf region.

In the run up to the November election, the usual US party preferences among Gulf states were less pronounced. The region as a whole shifted toward partisan non-alignment. Republican-leaning Saudi Arabia and the UAE appeared less enthusiastic about a Trump win than they were in 2016. And Oman, Kuwait, and Qatar tacked away from the Democratic Party, in light of widespread regional opposition to the Biden-Harris administration’s support for Israel’s bombardment of Gaza and Lebanon.

Two main factors sit behind the shift in preferences. First, Trump’s first-term record was spotty when it came to US support for the interests of the Gulf Cooperation Council (GCC) states. Their initial pro-Trump bonhomie faded when his administration failed to invoke the so-called Carter Doctrine—which calls for a US military response to any outside attempt to gain control of the Gulf region that threaten US national interests—in the wake of the 2019 drone and missile assault on Saudi Arabia. The Iranian-backed attack struck the Khurais oilfield and, more important, knocked out nearly six million b/d of oil processing capacity at Abqaiq, causing the largest-ever outage in the history of the oil business. For the Gulf, it seemed that Trump’s transactional approach to foreign relations allowed the United States to sidestep long-held commitments when they clashed with other priorities.

Trump’s first-term record was spotty when it came to US support for the interests of the Gulf Cooperation Council states.

Second, the Biden administration’s relationship with Saudi Arabia went in the reverse direction. Early rancor between Riyadh and Washington, especially after the Saudi-led OPEC+ oil production cut of two million b/d in 2022, soon gave way to pragmatism. Course corrections in US diplomacy with Saudi Arabia and the UAE eventually moved back toward friendlier relations.

Under Biden, Israel-Saudi normalization talks became a forum for sprawling—and still unfinished—US-Riyadh discussions toward a major upgrade in relations based on big concessions by both sides. Saudi recognition of Israel was just one aspect of a proposed broader US-Saudi strategic partnership that included an agreement by Riyadh to retain the US dollar in oil sales, curb strategic relations with China, and reject membership in the BRICS group of nonaligned developing states. In return, Saudi Arabia was to be placed under a formal US defense agreement and to receive US nuclear assistance on much more permissive terms than those achieved by the UAE in 2009.

Trump, who forged the 2020 Abraham Accords normalizing relations between Israel and four Arab states including the UAE, is expected to redouble efforts to bring Saudi Arabia and Israel into diplomatic ties. One imagines that even deeper concessions will be on offer if Riyadh is willing to forego its prerequisite of an independent Palestine.

US-UAE relations underwent a similar trajectory under Biden. A deadly Houthi attack on Abu Dhabi in 2022 created initial and deep distrust among UAE leadership toward the Biden administration and in US defense commitments. But by the end of Biden’s term, the two governments had signed a major defense pact. UAE President Mohammed bin Zayed met with Biden in Washington in 2024; he was the first UAE president to visit the White House.

Trump Challenge to China and Iran Less Welcome Than in Years Past

Trump’s preferences for harder lines on Iran and China both run counter to current preferences among US friends in the Gulf. The UAE, Saudi Arabia, and the rest of the GCC have for years steadily expanded cooperation with Beijing. And where Trump’s animosity toward Iran was welcomed by Abu Dhabi and Riyadh during his first term, a recent turnaround in Gulf-Iran ties makes a revival of the old Trump approach less appealing.

China trade ties have become the keystone of the Gulf economies, burgeoning relentlessly over the past two decades alongside increased Chinese demand for Gulf oil and gas. Gulf national oil companies including Saudi Aramco, the Abu Dhabi National Oil Company, and Kuwait Petroleum have, for more than a decade, recycled export earnings by plowing them back into investments in China and neighboring countries, building or buying stakes in refineries and petrochemical plants. These are considered strategic hedges, providing guaranteed sources of demand for Gulf oil and gas if global markets are oversupplied.

Chinese-Gulf ties have broadened beyond fossil fuels. Gulf-based power developers ACWA Power (Riyadh) and Masdar (Abu Dhabi) have entered joint ventures with Chinese engineering and renewables firms, erecting giant renewable power arrays in the developing world. Some of these generate—or will generate—electricity in underserved markets viewed as risky for foreign investment, avoided by western capital.

America’s friends in the Gulf have repeatedly said that they want to remain friendly with both Beijing and Washington.

Ironically, US and EU tariffs on Chinese solar panels unintentionally helped enable the China-GCC ventures. The trade restrictions contributed to a glut of cheap Chinese hardware, particularly photovoltaic (PV) solar panels, that lowered capital investment requirements. Normally low-return PV solar projects have become more profitable. In short, Gulf policymakers view their relations with China as vitally important. America’s friends in the Gulf have repeatedly said that they want to remain friendly with Beijing and Washington. They are loath to “choose sides” even if Trump demands it. (Of course, Gulf cooperation with China on military or communications network hardware would bring strong pushback under any US president.)

On Iran, Gulf-US misalignment also looms. Biden was keen to lower the temperature with Iran through a “less-for-less” policy of reducing US enforcement of sanctions on Iranian oil exports in exchange for reduced Iranian mischief around the Strait of Hormuz. Trump appears likely to re-tighten sanctions. Iran hawks Sen. Marco Rubio (R-FL), nominated by Trump to be secretary of state, and Brian Hook—chosen to lead the transition team for the Department of State—are overseeing hiring for the Department, which is a good indication of things to come.

Even as the incoming administration readies to revive pressure on Tehran, America’s Gulf partners are headed in the opposite direction. Saudi Arabia and the UAE, until recently the GCC’s most Iran-antagonistic countries, have made concerted efforts to improve relations. Their aim is to “de-risk” the potential for an Iranian attack on their territory in response to Israeli-US assaults on Iran. For Saudi Arabia, avoiding war is crucial to attracting foreign investment to its Vision 2030 diversification projects.

Meanwhile, the Gulf’s more Iran-friendly states—Qatar, Kuwait, and Oman—continue to engage Tehran. Oman has built its Iran friendship into a major diplomatic asset, emerging as a mediator that has calmed cross-Gulf tension.

All that said, tighter US sanctions on Iran might bring benefits for the GCC oil exporters. A revival of Trump’s “maximum pressure” campaign could take roughly one million b/d of Iranian exports off the global oil market. Such a loss of supply might lift oil prices sufficiently to allow OPEC mainstays Saudi Arabia, the UAE, and Kuwait to release some spare capacity and boost exports.

Of course, Iranian leaders may view the loss of exports and associated revenue—and any benefits transferred to Saudi Arabia and the UAE—as a call to action. Détente with Riyadh and Abu Dhabi would be threatened. One suspects that Iranian market share would be distributed broadly among OPEC+ members to allay concerns about collusion.

Conclusion: Signals Are Murky

There is no clear signal on the oil market effects of the incoming Trump administration. Signs pointing to increasing oil supply include campaign pledges supporting the US oil sector by reducing regulation, easing issuing of permits and drilling access to public land and water, and overturning the Biden administration’s pause on LNG export licensing. Trump might also couple an LNG export boost with a campaign to pressure US allies to buy American LNG.

If American oil and gas sales cut too deeply into OPEC’s market share, a Saudi-led price war could break out. Oil supply would jump further while prices—and profits—drop. Offsetting factors include the likelihood of increased enforcement of sanctions on Iran and perhaps on newly resurgent production in Venezuela. Such moves could take one million b/d or more off an oversupplied global market, counterbalancing Trump’s supply-boosting policies.

Over the longer term, Trump could seek to revive flagging US oil demand, which peaked in 2005. Trump appears amenable to rolling back US support for competing technology, including electric vehicles and perhaps, renewable power.

Given the complementary Republican control of Congress, Trump and his allies could repeal parts of the Biden administration’s Inflation Reduction Act that codified these incentives. Beyond that, Trump could also push for rollbacks of US vehicle fuel efficiency mandates. All such actions would be bullish for US oil demand.

Trump’s unorthodox methods and unrestrained and unpredictable diplomatic style portend another bout of disruption to US and global norms. US partners in the Gulf now appear less enthusiastic about the same Trump get-tough policies that they supported during his first term.

As witnessed then, some of the maverick president’s overtures went nowhere, while others succeeded in galvanizing action among reluctant US partners and adversaries. Once again, US relations with the outside world are in for renewed turbulence. Traditional bonds and stances will be tested.

The views expressed in this publication are the author’s own and do not necessarily reflect the position of Arab Center Washington DC, its staff, or its Board of Directors.

Featured image credit: Shutterstock/Hamara; Flickr/The White House