In early March 2026, Iran effectively closed the Strait of Hormuz in response to the war launched by the United States and Israel, making it impossible for oil and gas to be exported from the Gulf without its agreement. The Hormuz blockage is the biggest market disruption in the history of the oil industry and delivered a major blow to the longstanding US-Saudi “oil for security” bargain that has endured in various forms since 1945.

The International Energy Agency (IEA) said that the closure has thwarted exports of around a fifth of global oil consumption, averaging about 20 million barrels per day (b/d) in 2025, most of which normally flows to Asia. Fifteen million b/d of that amount was crude oil, with refined products making up the remainder (Fig. 1). Four operational pipelines currently have the capacity to allow an additional 3.5 to 5.5 million b/d to bypass the blocked Strait, leaving a net shortage of 14.5 to 16.5 million b/d.

| Crude oil (including condensates) |

Products | Total | |

|---|---|---|---|

| Bahrain | 0.00 | 0.21 | 0.21 |

| Iran | 1.69 | 0.72 | 2.41 |

| Iraq | 3.32 | 0.31 | 3.63 |

| Kuwait | 1.40 | 0.97 | 2.37 |

| Qatar | 0.73 | 0.69 | 1.43 |

| Saudi Arabia | 5.43 | 0.80 | 6.23 |

| Saudi‑Kuwaiti Neutral Zone | 0.35 | 0.00 | 0.35 |

| United Arab Emirates | 2.02 | 1.22 | 3.24 |

| Total Hormuz | 14.95 | 4.93 | 19.87 |

Figure 1: Crude oil and refined product exports via Hormuz, in million b/d, in 2025 (Source: IEA 2026)

Another Casualty of the War: Spare Capacity

The US-Saudi special relationship has for decades provided the stability for a long period of development and economic growth which, in turn, produced copious benefits to the global economy. In exchange for Saudi Arabia and its neighbors supplying steady flows of oil to energy importers, the United States (like the United Kingdom before it) provided the hard security protection that allowed oil to be shipped through strategic maritime chokepoints such as the Strait of Hormuz.

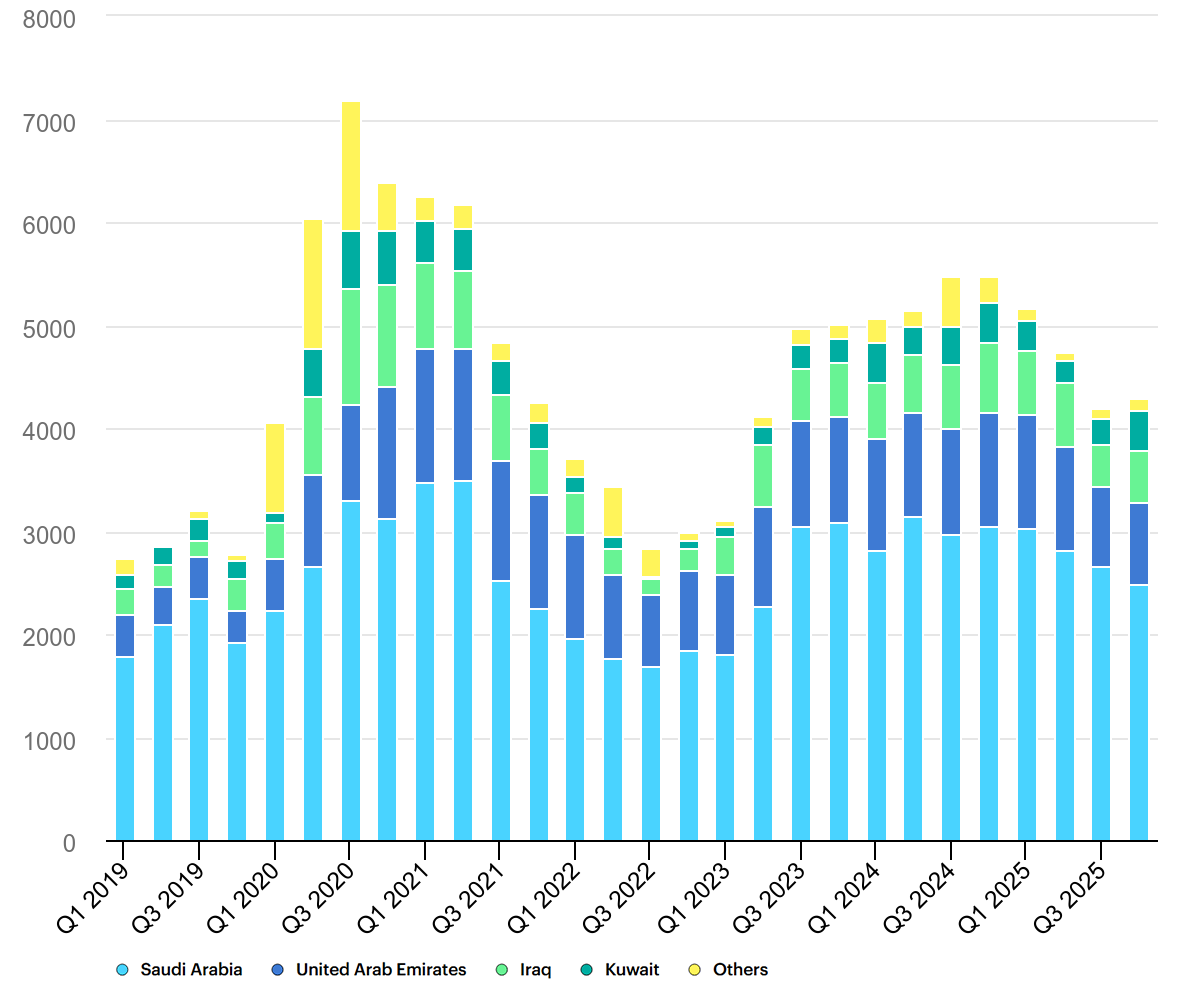

The stability that underpinned this arrangement has now vanished. Disappearing alongside it is the world’s access to spare oil production capacity, which is the oil market’s main shock absorber. The Hormuz crisis has locked away about 4 million b/d in excess capacity held by Iraq, Kuwait, Saudi Arabia, and the United Arab Emirates (UAE) (Fig. 2), which acts as the market’s “relief valve” when crises strike. In the current emergency, that relief valve is unavailable because it is also trapped in the Gulf behind the Iranian blockade.

Figure 2: Just over 4m b/d of spare oil production capacity at the end of 2025 was held in countries that export via the Strait of Hormuz, including Saudi Arabia (lt. blue), the UAE (dk. blue), Iraq (lt. green), and Kuwait (dk. green). Others (yellow) include the rest of OPEC-13 but excludes Iranian and Venezuelan crude under sanctions. (Source: IEA 2026)

Supply Chains Beyond Oil Are Also in Crisis

The Hormuz closure is not just throttling shipments of oil. There is also no liquefied natural gas (LNG) flowing (normally 20 percent of world supply would transit through the Strait), and little or no sulfur, helium, aluminum, petrochemicals, polymers or resins, urea, ammonia, or liquefied petroleum gas (LPG). All are bottled up inside the Gulf, unable to flow out the Strait of Hormuz.

Effects from this trade stoppage have spread far and wide. Each of these commodities sustains supply chains of complex goods and services. Losing them triggers knock-on effects and higher prices. With less helium available, semiconductor and fiber optic cable manufacturing has stalled. With less sulfur, computer chips cannot be etched. With less urea, sulfur and ammonia, the supply chain to produce fertilizer has been choked off, which means crop yields could suffer and prices could rise.

The closure of Hormuz demonstrates that the Gulf is one of the world’s main resource regions, touching nearly every life on the planet. Access to the Strait should therefore be maintained by all, but it requires political stability to function. If just one of its eight stewards (Bahrain, Iran, Iraq, Kuwait, Oman, Qatar, Saudi Arabia, and the UAE) is sufficiently aggrieved, it is now painfully apparent that that country can block the other seven from supplying the world, and from being supplied in return.

The Asymmetric Simplicity of Blocking Hormuz

Iran’s closure of the Strait of Hormuz was both easier and had a bigger impact than many observers imagined, for two reasons.

First, at the outset of the war, shipping insurance carriers in London contributed to dissuading transit through Hormuz by invoking war risk clauses. Shipping paused while actuaries reformulated pricing that accounted for the new risks.

Second, the pause in shipping became a halt when Iranian attacks on vessels made those risks real. On March 1, 2026, Iran began to strike civilian shipping in and around the Strait of Hormuz, killing two people and injuring four when it hit the tanker Skylight off Oman. As of March 24, Iran had hit more than 20 ships (Fig. 3). Daily transits have dropped from an average of 135 to just 10.

Figure 3: Locations of confirmed attacks (in red) and incident reports (yellow) since February 28, 2026, in and around the Strait of Hormuz (Source: UKMTO 2026).

Private insurance brokered in London has since priced the risk, with Hormuz coverage rising from around 0.25 to 0.5 percent of the vessel value per transit to 5 percent or more. The Trump administration has deputized the US Development Finance Corporation to step into the breach with subsidized reinsurance coverage for shippers willing to run the Hormuz gauntlet. At some point, naval escorts provided by willing countries are supposed to assist vital cargoes in passing the strait.

Whether ships can traverse the Strait during active combat remains unknown. In normal times, the 29-mile-wide passage maintains twin two-mile-wide navigable channels, one for inbound and one for outbound shipping, with a two-mile-wide buffer zone separating them. There is little room for navigational error or evading attack. Industry members estimate that US-subsidized reinsurance may help around the margins by increasing the profits that risk-tolerant shippers can earn by being willing to run the Strait. Inevitably, some will try it.

Alternative Solutions

Iran is offering an alternative to risking the Strait. For shippers seeking to travel to Iran-friendly destinations such as China, India, Malaysia, or Pakistan, there is restricted passage along Iran’s shore that allows for Iranian inspection and in some cases, payment. Recent transits along these lines include Indian LPG tankers using a “pre-approved” route after diplomatic discussions with Tehran. Japanese authorities have announced a similar deal for Japan-bound cargoes.

This approach mirrors the 2023–2025 Houthi strategy used in the Bab al-Mandab and the Red Sea, which effectively turned a global maritime commons into a firing zone that stopped only for friendly shippers without links to the United States, Israel, or Europe. The Houthis’ actions amounted to a form of economic sanctions on countries friendly to Israel.

Widespread opposition to the US-Israeli war on Iran may provide more shippers and governments a rationale to consider the Iranian option. Like the Gaza war that prompted the Houthi attacks, the US-Israeli war on Iran is exceedingly unpopular. Only in Israel do surveys show public support for the war at over 50 percent. In the United States, the war is the least popular of all US wars at their outset. International willingness to stand up to the Trump administration also appears to be gathering pace; governments may be pushed by urgent economic pressures to make the case for a different approach to Iran.

Lasting Damage

In the longer term, however, Iran’s actions could have lasting damage, possibly turning what used to be part of the global maritime commons into an Iranian-controlled fee-for-use waterway. In such a scenario, Tehran would reap a new revenue source while locking in additional transport costs on top of an already inflationary global economy. It is likely that many countries eventually would oppose such Iranian control, but the specter of persistent trade restrictions provides Iran with negotiating leverage in the short term.

As is often the case in warfare, the weaker combatant benefits from asymmetry. The task of forcibly reopening the Strait and protecting 100 transits a day is orders of magnitude more difficult than Iran’s tactics of making threats, laying mines, and launching inexpensive kamikaze drones that only occasionally hit their targets. Many observers believe that forcing open Hormuz would require a US ground invasion. Even then, Iran has other options for escalating its retaliation: Halting desalination and electricity production in US-allied Gulf Arab countries, blocking the Bab al-Mandab and Saudi oil flows to Asia, striking Hormuz bypass pipelines, or destroying further valuable and complex oil and gas export infrastructure.

New Gulf Security Architecture?

By closing Hormuz and creating worldwide commodity shortages, Iran is forcing the United States and Israel to shorten their time horizons, to escalate the war with a ground invasion, or to drop their objective of regime change. But the United States and Israel need more time to achieve Israel’s war aims of destroying the Iranian regime (the Trump administration’s war aims are unclear).

What happens to oil-for-security when the fighting stops? Before the war, the US security umbrella was already fraying. The United States failed to prevent the September 2025 Israeli strike on Doha or the September 2019 Iranian strike on Saudi Aramco’s Abqaiq facility. Under the Trump administration, the US security force in the Gulf has transitioned from protector of trade to instigator of war. As a result, US military bases in the Gulf are now Iran’s key targets. When calm returns, Gulf countries will face a difficult reassessment of the growing risks of relying on US security provision.

The views expressed in this publication are the author’s own and do not necessarily reflect the position of Arab Center Washington DC, its staff, or its Board of Directors.

Featured image credit:Tommy Chia SG/Shutterstock